How much has been invested in savings bonds this year?

The American public invested $NaN million in savings bonds this fiscal year to finance the federal government.

Fiscal year-to-date (since October ) total is updated monthly using the Electronic Securities Transactions dataset.

Compared to the same period last year (Oct -1 - Invalid Date ), investments in savings bonds have .

Key Takeaways

Savings bonds are simple, safe, and affordable loans to the federal government that can be purchased by individual investors. These loans help finance the government and offer benefits to the purchaser.

The level of investment in savings bonds has varied over the course of American history. In some cases, the government has developed public campaigns to promote savings bond purchases in an effort to fund activities such as the country’s participation in World War II. At other times, sales of savings bonds have increased or decreased in tandem with changes in interest rates or inflation.

Savings bonds earn interest until they reach "maturity," which is generally 20-30 years, depending on the type purchased. If a bond is held past its maturity, the federal government remains responsible for the debt. However, savings bonds that are held past their maturity date do not continue to earn interest and may actually lose value due to inflation.

Savings Bonds Overview

U.S. Treasury savings bonds are a type of loan issued by the U.S. Department of the Treasury (the Treasury) to individual investors. They are low-risk, interest-bearing securities that individual investors can purchase directly from the government on TreasuryDirect. Savings bonds are designed to offer a safe investment opportunity to ordinary Americans with the hope that by owning shares in their country, they may become more interested in national policy.1Wondering how much your savings bond is worth today? Visit the Savings Bond Calculator to find the value of your paper bonds or log in to your TreasuryDirect account to determine how much your electronic bond is worth.

How Do Savings Bonds Help Finance the Federal Government?

The government finances programs like building and maintaining roads, school funding, or support for veterans through revenue sources like taxes. When the government spends more than it collects from revenue, this results in a deficit, which requires the government to borrow money (debt) by issuing loans (securities) that it promises to pay back with interest. Different types of securities earn interest in different ways. Treasury groups securities into two categories called marketable and non-marketable securities, which reflects whether they can be resold to another individual or entity after they are purchased.

Savings bonds make up % of total debt held by the public through . This is percentage points the percent of debt held by the public ten years ago (%).

Types of Savings Bonds

Over the course of American history, the U.S. government has issued savings bonds to help fund certain programs and special projects like the space program. Each bond type has different terms and ways that it earns interest. Today, there are two types of savings bonds available for purchase: Series I bonds and Series EE bonds.What Influences the Purchase of Savings Bonds?

Public demand for savings bonds has varied over time. Changes in interest rates or inflation can make bonds an attractive investment relative to other alternatives. In addition, investors may be motivated by the idea of supporting a national cause like a war effort or government project.

Savings Bonds History

The sale of U.S. Treasury marketable securities began with the nation’s founding, where private citizens purchased $27 million in government bonds to finance the Revolutionary War.2 These early loans to the government were introduced to raise funds from the American public to support war efforts as well as other national projects like the construction of the Panama Canal.

During the Great Depression, the U.S. government sought to stabilize the economy by issuing a new type of Treasury security: savings bonds. In 1935, savings bonds were first introduced to promote thriftiness and allow individuals to purchase government-backed bonds at an affordable price. For many decades, the minimum purchase price for marketable securities was several thousand dollars, which meant that only very wealthy individuals and institutions could afford to invest in them. With the introduction of the first savings bonds, regular citizens were able to invest in Treasury securities, and they gained popularity as a “safe haven” during times of economic uncertainty.

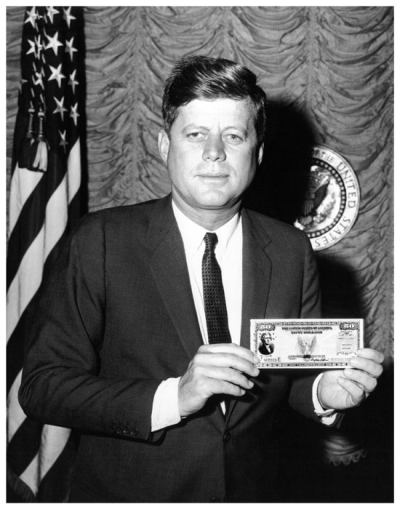

In 1963, President John F. Kennedy aimed to encourage the purchase of savings bonds by establishing the U.S. Industrial Payroll Savings Committee. This committee encouraged workers to automatically invest a portion of their paycheck in what was known as the Payroll Savings Plan, which reduced paper certificates, and moved to an electronic record-keeping system. This new program was accompanied by nationwide marketing and helped increase the profile of the savings bond program in subsequent decades.

The chart below shows savings bond sales over time for all savings bond types.

Savings bonds were most popular in and when $0 M and $0 M bonds were sold, respectively.

Interest Rates and Inflation

The economy can also influence the popularity of investing in savings bonds. In times of heightened economic uncertainty, individual investors may favor savings bonds due to their low risk, even if they produce a more modest return. Conversely, economic growth may create attractive investment opportunities outside of savings bonds, where individual investors may be able to earn higher interest rates.

In general, when interest rates are higher, demand for fixed-rate savings bonds like Series EE tends to increase. However, when people expect inflation to increase, savings bonds like Series I become attractive because they provide protection against inflation, preserving the value of the money invested. In the spring of 2021, inflation in the United States began to rise over three percent and would grow to over six percent by September 2022. In response, the American public invested heavily in Series I bonds, purchasing nearly $153 billion of Series I bonds between April 2021 and February 2023. The chart below shows inflation data and I bond purchases from the last 15 years.

Generally, higher inflation rates are correlated with an increase in demand for inflation-protected securities like I bonds.

What Happens when Savings Bonds are Fully Matured?

A savings bond can be redeemed anytime after at least one year; however, the longer a bond is held (up to 30 years), the more it earns. When a savings bond is redeemed after five years, the owner receives the original value plus all accrued interest. If a bond is redeemed before five years, the holder loses the last three months of interest.

Occasionally, bond owners hold onto bonds after they have reached maturity and are no longer earning interest. These outstanding but unredeemed bonds are called Matured Unredeemed Debt (MUD). The government continues to be responsible for this debt, as it may be redeemed at any time. Therefore, the Treasury has increased efforts to encourage bondholders to redeem their matured savings bonds. As of January 1970, there were NaN million matured unredeemed savings bonds held by investors.

If bonds are held past their maturity date, the bonds can lose value due to inflation. To understand how this value is lost, see the illustration below.

Could there be a savings bond in your name that you might not know about? Go on a Treasure Hunt and see what bonds might be waiting for you to cash in!

Learn More: Buying and Redeeming Savings Bonds Today

Today, individuals can buy Series I and Series EE bonds online through TreasuryDirect. TreasuryDirect also offers a feature called Treasury Hunt, which allows users to search to see if there are unredeemed bonds in their name.